We analyzed 7,000 Southeast Asian banking app reviews. Here's the churn risk hiding in them.

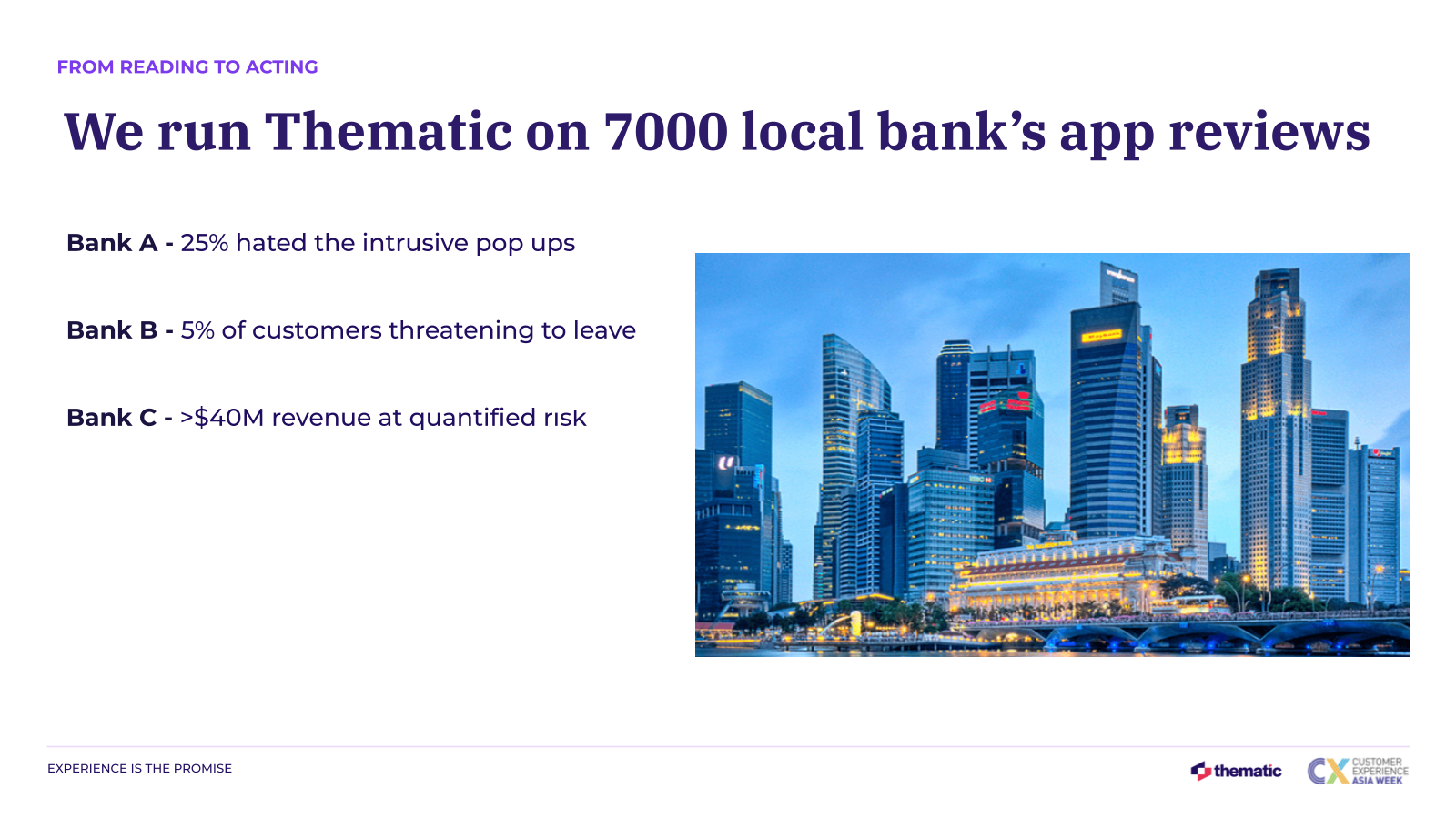

Thematic ran 7,000 Southeast Asian banking app reviews through its Scoring and Theming Agents. The findings: a pop-up backlash at one bank, switching intent at another, and more than SGD 40 million in churn risk at a third.

Thematic analyzed 7,000 app store reviews of Southeast Asian banks and found churn risk hiding in plain sight: 1 in 4 reviewers annoyed by pop-ups at one bank, 5% signaling switching intent at another, and over SGD 40 million in revenue at risk at a third. App reviews caught what quarterly surveys, which sample about 7% of customers, could not. The article shows how any bank in the region can run the same analysis.

At one Southeast Asian bank, more than SGD 40 million in revenue is at quantified risk of churn. The warning is not buried in a boardroom dashboard or a quarterly relationship survey. It sits in public view, in the bank's own app store reviews, where anyone can read it.

Thematic analyzed 7,000 app store reviews of local banks across Southeast Asia, in research presented by co-founder and CEO Dr. Alyona Medelyan at CX Asia in Kuala Lumpur. The reviews were treated as the survey customers never filled out. Thematic's Scoring Agent predicted how each reviewer would rate the bank on the promises banks compete on: ease, reliability, value, fairness, and empathy. Thematic's Theming Agent surfaced what moved each score up or down. No survey was sent, and no customer was interrupted.

The findings were specific enough to act on the same week. At one bank, a quarter of reviewers complained about intrusive pop-ups in a single month. At another, 5% of reviewing customers said outright they were ready to switch banks. At a third, the revenue attached to churn-signalling customers exceeded SGD 40 million. This article walks through the three findings, explains why survey programs miss signals like these, and shows how any bank in the region can read the same risk in its own reviews.

Southeast Asia's banking went mobile. The feedback went with it.

Southeast Asia is one of the most app-dependent banking regions in the world. McKinsey's Personal Financial Services survey found that active digital banking use in Asia-Pacific's emerging markets jumped from 54% in 2017 to 88% in 2021. By 2021, roughly nine in ten consumers across the region were using digital banking actively. The e-Conomy SEA 2024 report from Google, Temasek, and Bain put digital financial services revenue in the region at USD 33 billion in 2024, up 22% in two years.

The regulators tell the same story country by country:

In Malaysia, mobile banking now accounts for 62% of online banking transactions, up from 50% a year earlier, according to Bank Negara Malaysia's 2024 Annual Report.

In the Philippines, digital payments reached 57.4% of retail transaction volume in 2024, beating the national target, per Bangko Sentral ng Pilipinas.

When the app is the branch, the app store becomes the complaint desk. Every one-star review is a customer explaining, in their own words and in public, why they might leave. And leaving is realistic: in McKinsey's 2021 survey, around 60% of Asia-Pacific consumers said they would consider switching to a branchless, digital-only bank.

Banks in the region know experience is the battleground. In PwC's Southeast Asia digital banking survey, 68% of banks named improving customer experience as the primary driver of their digitalization programs. The same survey found more than 80% had not yet achieved their digitalization goals. The gap between intent and execution is exactly where churn risk accumulates.

What did 7,000 reviews reveal at three banks?

The analysis Thematic presented at CX Asia covered app reviews of local banks, scored against the promises every bank makes. Three findings stood out, one per bank. The banks are anonymized here, as they were in the original analysis.

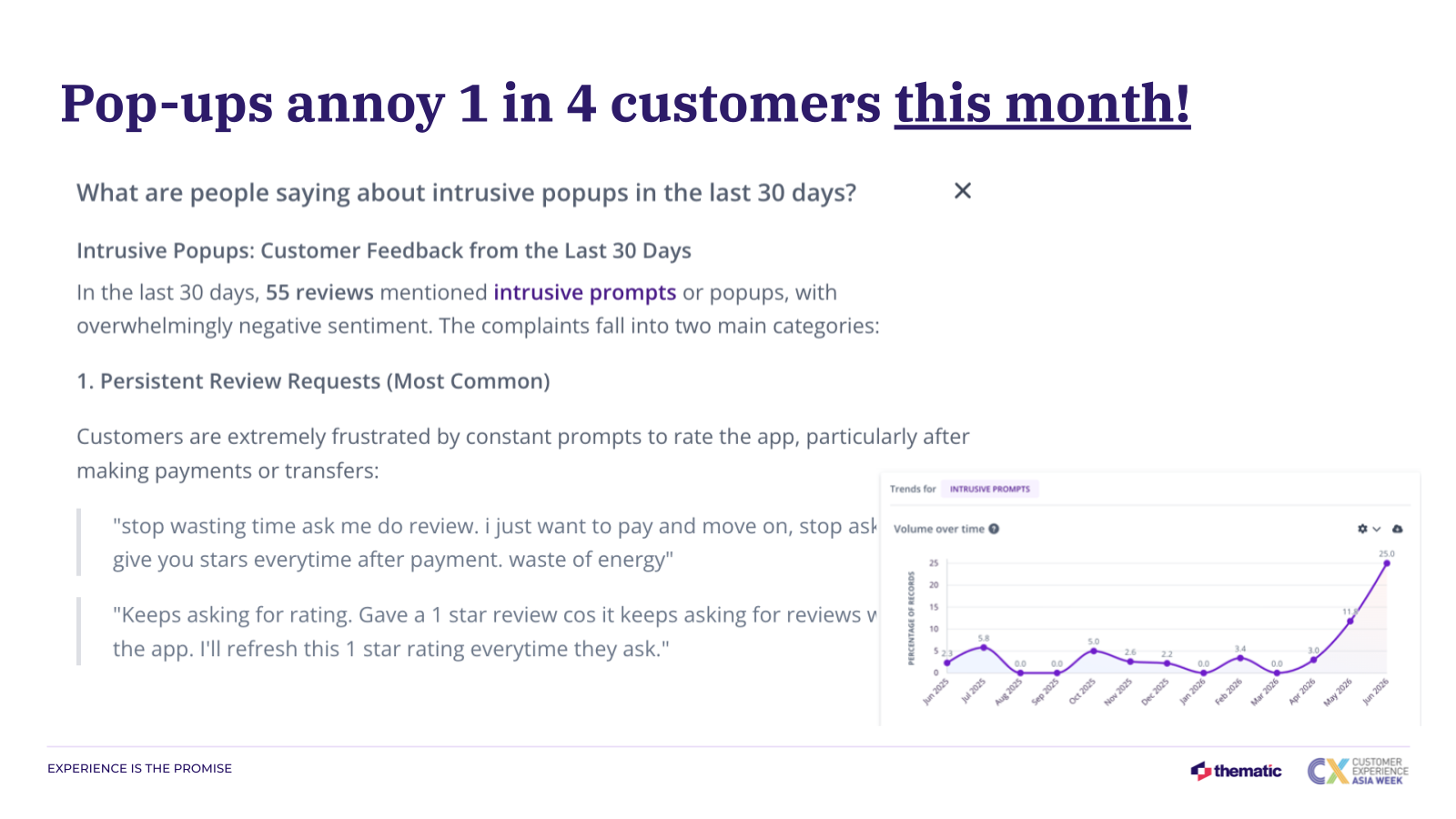

Bank A: pop-ups annoyed 1 in 4 customers in a single month. At one bank, 25% of reviewers in one month complained about intrusive in-app pop-ups. This is a self-inflicted wound: promotional interruptions inserted into a task customers want to finish in seconds. It is also among the cheapest churn drivers to fix. The bank controls it end to end, with no competitor action, rate change, or regulation involved.

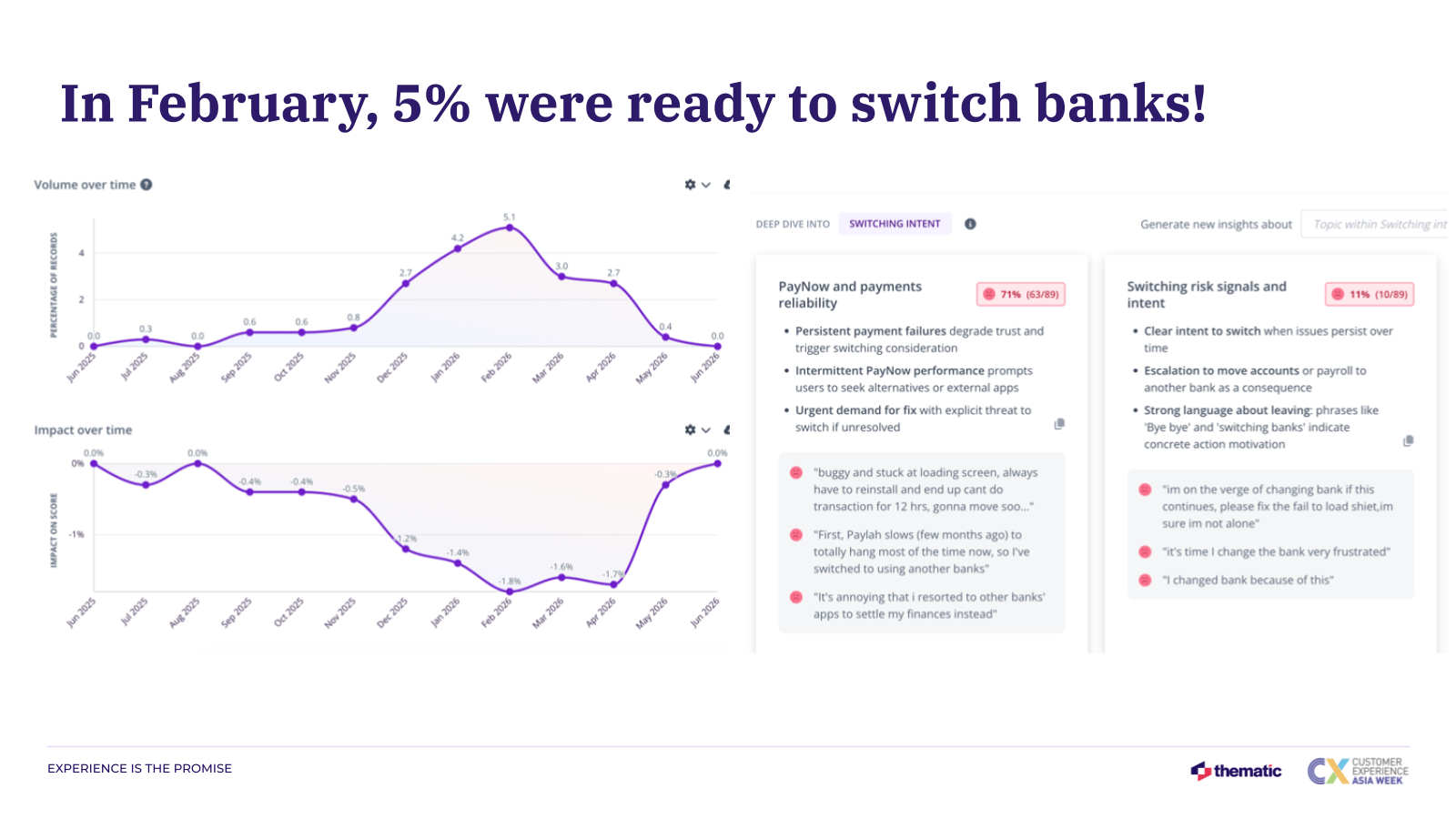

Bank B: 5% of reviewing customers were ready to switch. In February, 5% of one bank's reviewers stated switching intent: not vague frustration, but comments that named leaving as the next step. Switching intent is a theme you can count, trend, and alarm on. A bank that only tracks its average star rating would never see it, because averages flatten exactly this kind of polarized signal.

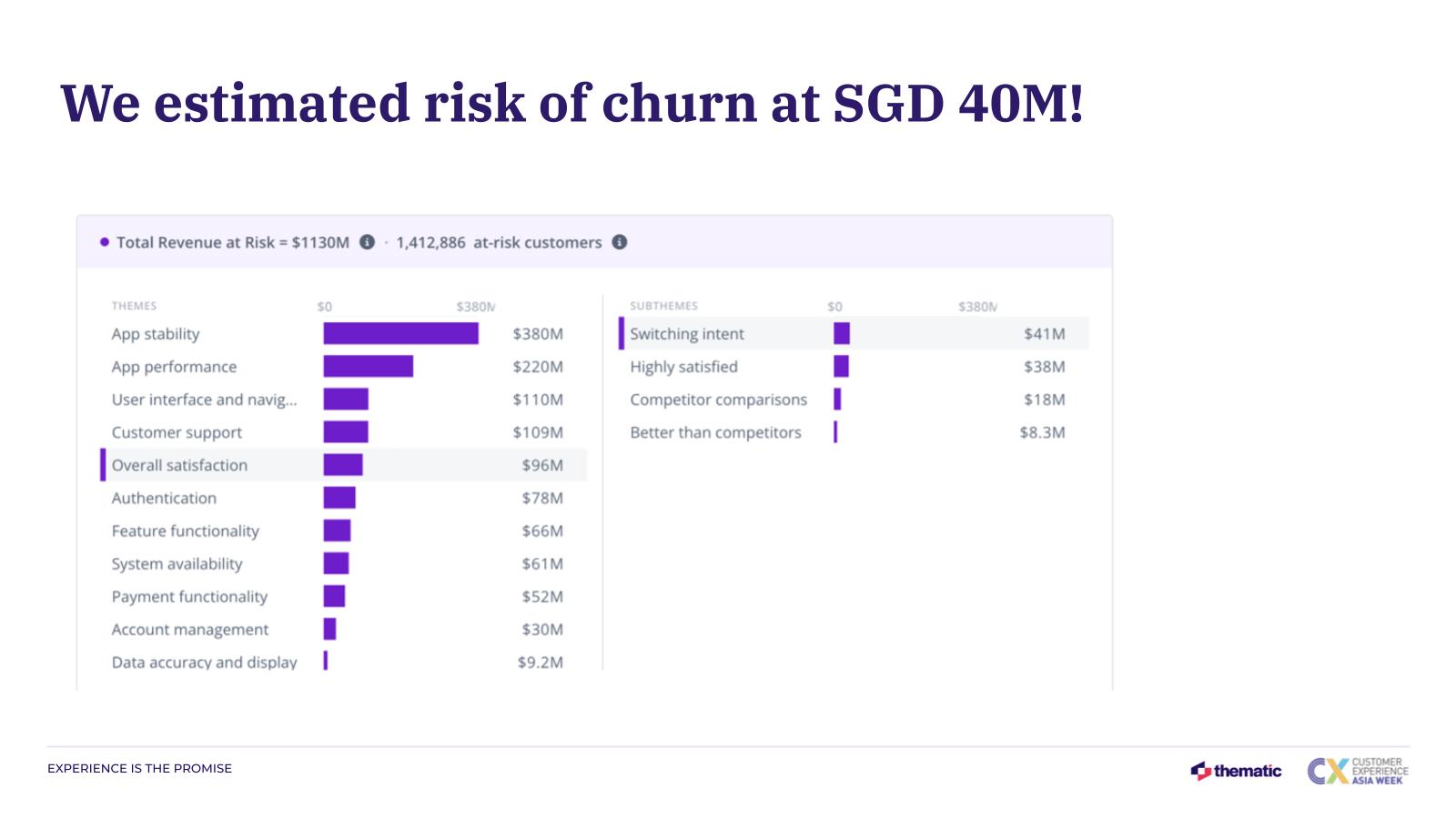

Bank C: more than SGD 40 million in revenue at quantified churn risk. The most consequential finding was not a complaint theme but a number. Reviewers whose predicted value score sat at the bottom of the scale are the churn signal: a customer who scores a bank's value at 1 is telling you the relationship is failing. Attach the share of at-risk reviewers to revenue per customer and churn risk stops being a sentiment and becomes a line item. At this bank, the line item exceeded SGD 40 million.

The pattern across all three: the signal was public, current, and specific, and none of it required sending a survey.

Why do survey programs miss this?

Most banks in the region already run NPS or CSAT programs. The problem is coverage and speed, not intent.

McKinsey's research on CX measurement found the typical survey samples only 7% of a company's customers, and only 13% of CX leaders were fully confident their measurement gives a representative view. Meanwhile 93% of CX leaders rely on survey-based metrics as their primary measure, and only 15% are fully satisfied with them. A quarterly survey of a small sample cannot catch a pop-up backlash that builds in four weeks, or a switching-intent spike in February.

App store reviews invert every one of those constraints. They are unsolicited, so they capture customers the survey never reached, including the angriest ones. They are continuous, so a monthly spike is visible as a spike. And they are public, which cuts both ways: prospective customers read them, and so does everyone else's AI assistant. Acting on them pays directly too. Google's own Play Console data shows that responding to a negative review lifts that rating by an average of 0.7 stars.

Surveys still matter for depth and for tracking relationships over time. But in a region where the app is the primary channel, treating app reviews as the leading indicator and the survey as the lagging one matches how customers actually behave.

Reading churn risk at scale is a scoring problem, not a reading problem

No insights team reads 7,000 reviews, and skimming produces anecdotes rather than numbers. The approach behind this analysis works in two layers.

First, scoring. Thematic's Scoring Agent predicts, for every review, how that customer would have rated each promise attribute if they had been surveyed: synthetic survey responses grounded in data the bank already owns. This is the same approach Thematic used to show that customer feedback predicted Spirit Airlines' collapse more than a year in advance. The score makes reviews trendable and comparable across banks and months.

Second, theming. Thematic's Theming Agent finds what drives each score up or down, so a falling value score resolves into "intrusive pop-ups" or "transfer fees" rather than a red number with no explanation. The score tells you something changed. The theme tells you what to fix.

One caution belongs here, because the same experiment is easy to run badly. A general-purpose AI model pointed at reviews will happily produce findings, but ungoverned AI invents numbers, gives a different answer every run, and cannot show its work. A churn-risk figure a bank cannot audit is a churn-risk figure the CFO will not act on. If a system cannot be trusted, it will not be adopted. Whatever tooling a bank uses, the requirements are the same: consistent scores across runs, themes traceable to the underlying quotes, and numbers that can be recomputed.

The payoff for getting this right shows up in operators who acted. Orion Air, a low-cost carrier in the Asia-Pacific region, sends customer verbatims, NPS scores, and contextual metadata into Thematic. It found that 80% of its top customer issues were operationally fixable, and acting on them drove a 13% increase in NPS. Atom bank, the UK's first app-only bank, analyzes app store reviews alongside six other feedback channels in Thematic. It cut calls about unaccepted mortgage requests by 69% and grew its customer base 110% year over year. Different markets, same mechanism: read the unsolicited signal, route it to an owner, fix the driver.

How can a Southeast Asian bank run this on its own reviews?

The experiment is repeatable by any bank in the region. The steps:

Pull the last 12 months of reviews for your apps from both the App Store and Google Play, across every market you operate in.

Score every review against the promise attributes banks compete on: ease, reliability, value, fairness, and empathy.

Track the share of bottom-of-scale value scores monthly. That share is your churn signal, and its trend matters more than its level.

Quantify the exposure: multiply the at-risk share by average revenue per customer to turn the signal into a number your CFO recognizes.

Route each driving theme to the team that owns it, and respond to the negative reviews you fix. Google's data says the reply alone is worth 0.7 stars.

The SGD 40 million at Bank C was not hidden. It was public, timestamped, and free to read, and the same is true of whatever is sitting in your app's reviews right now. The banks that win the next five years in Southeast Asia will be the ones that read their feedback early and act while the problem is still fixable.

Want to see what your own app reviews are signaling? Book a demo and run the same analysis on your bank's data.

Share

Link Copied!

Request a demo of Thematic's Customer Intelligence Platform

Thematic turns fragmented feedback into one consistent source of customer truth — so every team acts on the same customer story. Up and running in days, not quarters.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.